Half-yearly Dealtracker – H1 2021

PublicationThis publication captures key M&A and PE deals from the first half of 2021

For more updates follow Grant Thornton Bharat on WhatsApp

By: Abhay Anand

19 Jul 2021 3 min read

The second wave of the coronavirus pandemic impacted the economy in H1 2021, however, the confined nature of lockdowns, better adaptation of people to work-from-home protocols, online delivery models, e-commerce and digital payments at work moderated the impact.

This led to M&A deal activity being almost unhindered and saw an increase both in the deal volumes from 163 deals in H1 2020 to 221 deals in H1 2021, which is 36% higher. Deal values in H1 2021 stood at USD 24.4 billion compared with H1 2020 that recorded USD 18.2 billion. However, this needs to be seen in context of Facebook’s and Google’s investment of USD 10.1 billion in Jio Platforms Ltd. in H1 2020.

While domestic M&A dominated in terms of volumes with 76% contribution to total M&A deals during H1 2021, value wise domestic M&A contributed 64% of total M&A deals only in H1 2021.

On the other hand, cross border M&A saw a severe fall in deal volumes; contributing only 24% of the total M&A deal volumes during H1 2021, which was the lowest recorded in the first half of any of the past years starting from H1 2011. Despite that, contribution to the M&A deal values was at 36% in H1 2021, which was primarily driven by Adani Group’s Acquisition of SB Energy India from Softbank Group in May of 2021.

Adani Group was one of the most active acquirers during H1 2021 having acquired five companies above USD 200 million value. Their acquisition of SB Energy India for USD 3.5 billion was the largest acquisition in the renewable energy sector in India, due to which energy and natural resources sector topped M&A values lead table in H1 2021.

The banking and financial services sector was tailing energy and natural resources sector by being the secon highest contributor to deal values during H1 2021. This was primarily driven by Piramal Group’s acquisition of DHFL for USD 5.1 billion under the Insolvency and Bankruptcy Code. This was also the largest M&A deal during H1 2021.

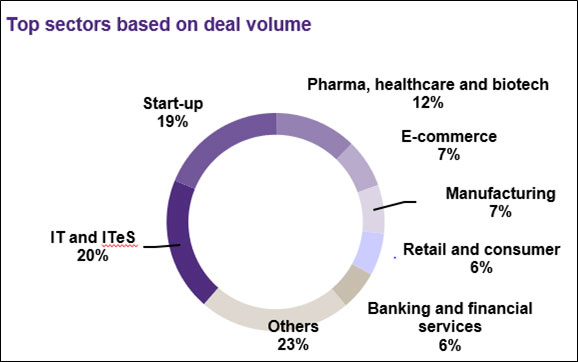

The IT/ITeS sector witnessed the highest number of M&A deals with 44 deals in the sector amounting to USD 2.5 billion (58% higher than USD 1.6 billion in H1 2020). This was driven by Wipro’s acquisition of Capco for USD 1.45 billion.

Transactions in pharmaceutical space saw a steep rise in terms of volume. It grew by 50% to 27 deals in H1 2021 as compared to 18 deals in H1 2020. Deal values on the other hand also doubled from USD 564 million in H1 2020 to USD 1.1 billion in H12021. The largest deal in the sector was Docon Technologies Pvt. Ltd.’s acquisition of Thyrocare Technologies Ltd. for USD 623 million.

Other key developments in H1 2021 also included one of the largest edtech acquisitions in the world of Aakash Educational Services by BYJU’s for USD 1.0 billion, which shows the potential of the Indian education sector primarily due to its large student demography and Tata’s acquisition of India’s largest e-grocery player BigBasket.com from Alibaba Group for USD 1.2 billion in the E-commerce Space.

Despite the hiccups and disruption caused from COVID-19’s second wave, there was an increase in deal volumes in H1 2021 compared with H1 2020, which indicates that the growth prospects of M&A activities look strong for H2 2021. Government’s increased focus on the vaccination programme in India and the positive outlook of the US economy should be conducive for more deal activities in the latter half of 2021.

Read more insights in our Half-yearly Dealtracker

The dynamic deal landscape requires expert intervention. Click here to know more or write to us at gtbharat@in.gt.com to connect with our experts.

This publication captures key M&A and PE deals from the first half of 2021

This publication captures key M&A and PE deals from May 2021

This edition of Dealtracker captures the deal activities in India for April 2021