PE, VC backed Indian firms eye SPAC listing

Media article

By: Raja Lahiri

21 Jul 20213 min read

Private equity (PE) and venture capital (VC) deal activity continued to be robust in H1 2021 despite the strong headwinds of the COVID-19 second wave that hit India in April and May 2021. PE and VC investments in H1 2021 were at USD 18.5 billion with 635 deals, higher than H1 2020, which witnessed investment of USD 17.6 billion and 440 deals.

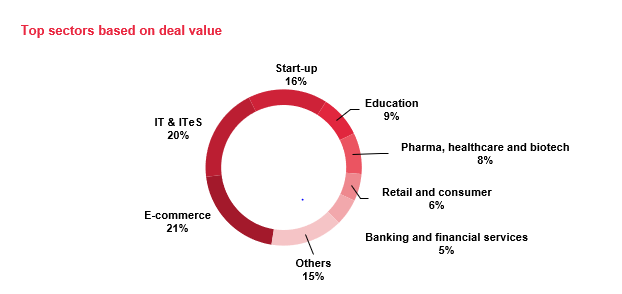

Digital and technology has continued to attract more than 50% of PE and VC investments across sub-sectors such as e-commerce, e-gaming, consumer tech, health tech, edtech and fintech. The other sectors of interest included healthcare and pharma, education, financial services and consumer.

Some of the notable deals included Blackstone’s additional investment into Mphasis, investments into Swiggy, Byju’s, Dream 11, FirstCry, Mesho, Infra market etc., as well as NIIF’s investment into Manipal Hospitals and Multiple PE’s buy-out of Zydus Cadilla’s animal health business.

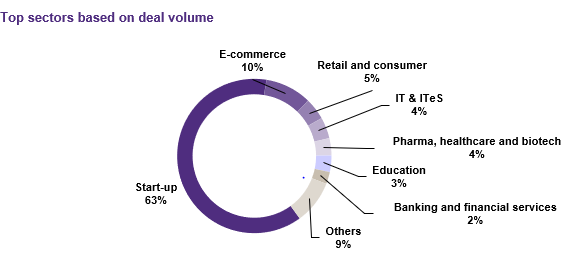

Rapid pace of unicorns in India

H1 2021 witnessed 10 new unicorns backed by strong PE and VC funding - Digit Insurance (Insurtech), Five Star Business Finance (NBFC), Meesho (social commerce), Infra.Market (B2B ecommerce), CRED (Fintech), Pharmeasy (Healthtech), Groww (Fintech), Gupshup (Conversational messaging), Mohalla Tech (parent company of social platforms ShareChat and Moj) and Moglix (B2B commerce).

We expect to see strong PE and VC deals in the new-age business models enabled by technology, and this augurs well for stronger Indian start-up ecosystems and one may witness a rapid growth of unicorns from India in 2021. Large M&A deals such as Tata’s acquisition of Bigbasket also demonstrates the strength of start-up ecosystem and demonstrates strong success for PE exit returns.

Read more about the deal landscape in our Half-yearly Dealtracker

The second wave had an impact on deal making and currently, PE and VC deal momentum has significantly gone up with number of deal negotiations and due diligence underway. This is perhaps driven by the deal pause that India witnessed during April and May 2021 and pent-up deal demand post this period. In my view, PE and VC capital will continue to flow in the new age sector companies to leverage the market opportunity in the digital business segment and provide capital to make acquisitions. This will drive deal momentum quite actively in the next six months of 2021.

We are also witnessing lot of interest from PE and VC backed Indian corporates for SPAC listing especially in the US capital markets and listing evaluation, planning and preparations are underway. While ReNew Power announced SPAC listing in 2021, there would be many more Indian companies that are expected to list overseas in the next six months of 2021. Clearly, this would augur well for PE/VC fund exits and typically, companies in technology and new-age sectors would see overseas listing interest such as SAAS players, e-commerce, renewable energy.

Given the strong stock market performance, India listings for PE backed companies also continue to be reasonably strong in 2021 such as Sona Comstar, Nazara Technologies, Kalyan Jewelers, Indigo Paints and more lined up in the next six months.

PE and VC funds continue to focus on portfolio company business and monitor operations closely and restructure and pivot business models given the uncertainty posed by the pandemic and the move to digital business models, with ESG focus.

The dynamic deal landscape requires expert intervention. Click here to know how we can show you the way forward

Listing a company in an overseas market is a long journey. Whether you want to go global now or later, our teams of experts can empower you. Click here to know how

Authors

-

Raja Lahiri

Partner & Overseas Listings Leader