5 ways you can safeguard your family business from fraud

Media article

By: Samir Paranjpe

16 Jun 2021 3 min read

All family offices & businesses have a go-to inner circle, comprising people we trust. In fact, one of the reasons for the success of family businesses is that they are founded on mutual understanding and cooperation. While trust plays an important role in family offices or family businesses, blind faith leads to susceptibility to fraud and abuse. It is, therefore, essential to achieve a balance between trust and oversight.

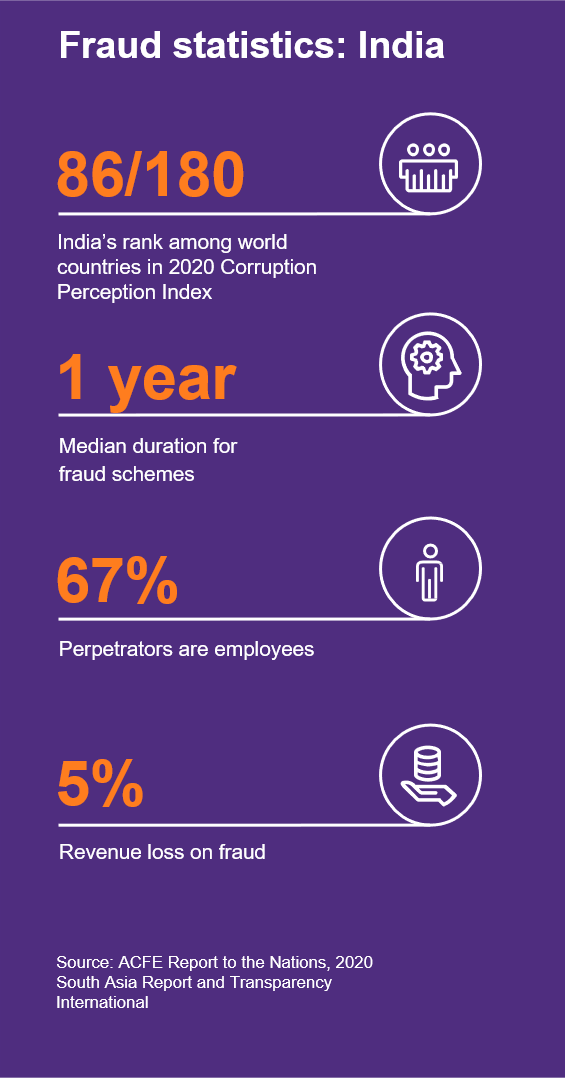

Family businesses contribute to 80 percent of GDP with an estimated net worth of $2 trillion. However, gradual expansion has also led to higher fraud statistics. According to the ACFE Report to the Nations 2020, 67 percent perpetrators are employees and at least one-third of frauds happen due to lack of internal controls in India. Let us now discuss some of the common fraud indicators.

Common fraud schemes and signs

A fraudster can either be a professional or an amateur insider and can use any of the following:

- Stealing: It is regarded as the oldest and the most common practice

- Conflict of interests: A conflict of interest sprouts when one’s personal interest outweighs the interest of the business.

- Diverting business funds: A black sheep often uses business funds to satisfy personal needs.

- Con artists: Conmen target UHNI families interested in investing in art and other aesthetic investments.

Fraud does not happen overnight and organisations must always be on the lookout for possible red flags, some of which are living beyond means, unusually close association with vendor/customer(s), excessive pressure within the organisation and defensiveness, control issues and unwillingness to share duties.

Faith, understanding and heritage can only offer a limited scope for growth. With changing times, it is essential to choose the right governance practice to mitigate fraud and ensure long-term business success. So, how does one ensure safety in family business? Here is what you can do:

Five things you can do to keep your business safe from fraud

- Due diligence: It is important to take reasonable care while appointing employees, especially the senior management, as they are the ones who hold power and confidential information. A thorough background and reference check before taking them on-board also helps, to an extent, in safeguarding your business.

- Fraud risk assessment: To understand a fraudster, it is essential to think like one! A fraudster is bound to exploit vulnerabilities in the system. Identifying those and filling the gaps can provide an extra layer of protection. This can be done by carrying out a stress-test for all the processes. This enables the management to identify risks and examine the adequacy of existing controls relating to prevention, detection and deterrence of fraud.

- Code of conduct: An essential step towards eradicating fraud is to acknowledge that all offices and businesses are susceptible to it, no matter how strong family relationships are. Thus, it is crucial to establish strong codes of conduct and create awareness about the same among employees. Sensitisation and regular communication related to the code can play an important role in preventing fraud.

- Whistleblower framework: Apart from relying on robust controls to prevent, detect and deter fraud, organisations must also adopt vigil mechanisms and a proper channel for receiving whistleblower tips and information. An appropriate whistle-blower framework, which is seen to be independent and credible, will encourage employees to come forward.

- Robust IT controls: It is essential to ensure that the IT controls of a firm are aligned with the realities of the day. Most companies tend to have a reasonably robust system in place. However, it is imperative to certify that these systems are fit for purpose and commensurate with the current scale and complexity of the organisation. Further, the IT controls must be deployed in a way that they complement monitoring and can detect anomalies to take proactive actions in relation to fraud and abuse.

With the right governance tools and systems, you can achieve business success along with strengthening family ties. Experts can help examine and audit financial statements and investment structure, conduct thorough fraud assessment using advanced technology and analytics tools, ensure compliance and documentation across geographies as well as identify vulnerabilities.

The article was published on Moneycontrol.

Authors

-

Samir Paranjpe

Partner and Leader, Forensic Investigation Services, Grant Thornton Bharat