Grant Thornton Budget Explainer: Over the last few years, 'cryptocurrency' has emerged as a hot investment topic, especially among young investors. Even the most avid investors, who have been traditionally putting money in safer avenues, have been bitten by the bug to explore this new digital asset.

So, if you are one of those people who have made investments or have been exploring 'cryptocurrency' as an asset class, the recent budget has put out some guidance paving clarity on how it will be taxed, yet there remain some stark question marks over how certain provisions will play out. For instance, whether a GST will be applicable. First things first, there have been a number of theories around Cryptocurrency, especially about its legal validity and the taxation play around it in the Indian context, some of which are still ambiguous. So, let's try to dig deeper to understand at what level the budget has now made the big canvas clear on Cryptocurrency.

Move on from PDA on Crypto: Govt now calls it VDA

If you're a 'cryptocurrency' enthusiast or investor, the budget has now clearly laid out a few guidelines and regulations pertaining to it. The Finance Minister Nirmala Sitharaman announced that there will be a tax of 30% on income from cryptocurrencies. For the taxation purpose, cryptocurrencies have now been included in the definition of Virtual Digital Asset (VDA).

For calculating such income only cost of acquisition is to be allowed as a deduction, which means no amount pertaining to any other expenditure (any transactional cost, interest cost of borrowing etc.) is allowed to be deducted. However, the basic exemption limit (Rs 2,50,000) is not applicable on income from transfer of cryptocurrencies.

However, if the transfer of VDA results in a loss, such loss can't be set-off against any other income, nor shall such loss be allowed to be carried forward to subsequent tax years.

For the uninitiated, VDA is a code or token (not being Indian currency or any foreign currency) generated through cryptographic means or otherwise, that provides a digital representation of value which is exchanged with or without consideration. VDA also includes non-fungible tokens (NFTs). NFTs are unique and non-interchangeable digital tokens which can be traded using cryptocurrency.

As such, the current regulations will impact your overall earnings from cryptocurrencies due to taxation imposed, but it also puts confusion and uncertainty to rest because the government has acknowledged cryptocurrencies as a VDA for taxation purposes and has created a framework for it.

Book profits before March 31: It’s highly taxable & still cryptic ahead

Since the new guidelines will come into effect from April 1 2022, the writing on the wall is very clear – unless you are very bullish on your crypto investments, liquidate them to book your profits now, so that you can explore options for saving potential taxes.

The taxation prior to 01 April 2022, is still ambiguous with a lack of clarity, but however the taxation may depend on the treatment adopted by the taxpayer. If the income from transfer of cryptocurrency is considered as business income, then the tax rate may still be similar, except there could be deduction of charges or expenses incurred.

If the income is chargeable as capital gains, then long term capital gain (where the crypto is held for more than 36 months) could be taxed at the rate of 20% and if the crypto is held for less than 36 months, then the taxation shall be as per the applicable slab rate for individuals.

Also, to regulate and capture details of transactions, taxes shall be withheld (TDS) on payment made to the seller of cryptocurrencies by the crypto exchange or any other payer at 1%, if the total payment during the tax year is above INR 10,000. These provisions are applicable from 01 July 2022 and primarily requires the crypto exchanges to deduct taxes, wherever required.

Also, gifting of VDA will be taxed in the hands of the recipient. Such taxability will arise only if the value of VDA exceeds Rs 50,000. But, there will be no tax liability in case of receipt of such assets through a relative as defined under the tax law or on the occasion of marriage etc.

While the step by the government to acknowledge and regulate cryptocurrencies through a taxation framework is a welcome step, there are still a few ambiguities, such as whether they are a valid legal tender, needs to be addressed and elaborated.

Illustration:

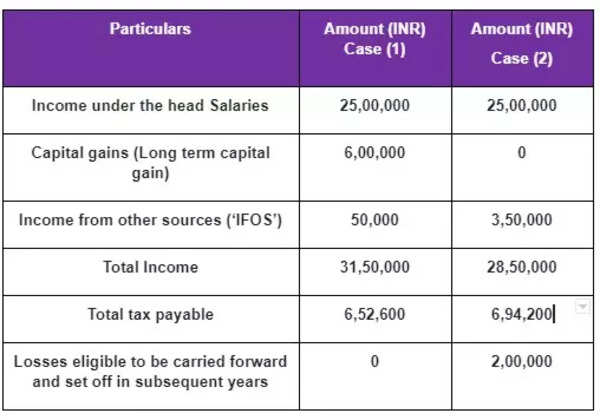

Mr. Ravi, a resident of Gujarat, is an employee working for an Indian IT company. Consider he has the following incomes for FY 2022-23:

- Income under the head Salaries – INR 25,00,000;

- Interest from bank fixed deposits amounting to INR 50,000;

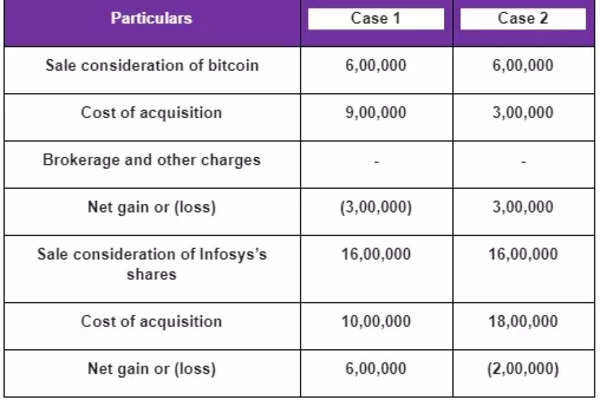

- He sold 1,000 shares of Infosys at 1600 per share on 30 Jan 2023 which he purchased on 20 December 2021;

- He sold bitcoins worth INR 600,000 on 30 Dec 2022 which he purchased on 12 Apr 2022; He gifted bitcoins worth INR 200,000 to his friend, Subhash on his birthday.

Consider the following:

Case 1: The cost of acquisition of bitcoin is INR 9,00,000 excluding brokerage and other charges of INR 10,000. Further the cost of acquisition of shares of Infosys is INR 1000 per share;

Case 2: The cost of acquisition of bitcoin is INR 3,00,000 excluding brokerage and other charges of INR 25,000. Further the cost of acquisition of shares of Infosys is INR 1800 per share; Let us now try to compute the total income and tax payable by Mr. Ravi for FY 2022-23/AY 2023-24:

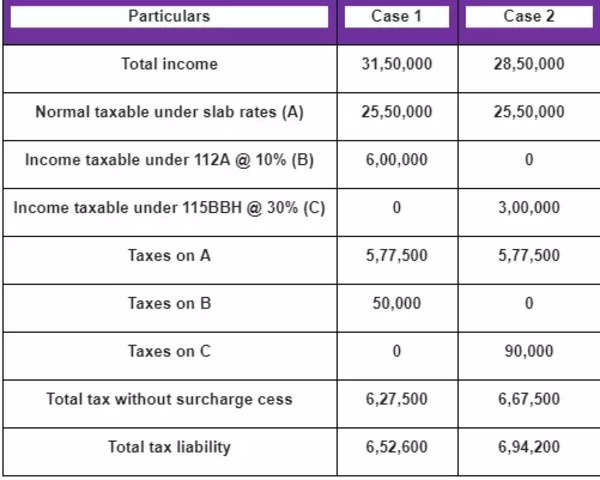

Calculation of total tax payable:

Notes –

1) Loss from transfer of any VDA cannot be set off against any other income. Accordingly in case 1, loss of INR 300,000 from sale of bitcoin is not set off against the gains of INR 600,000 from sale of shares of Infosys or from IFOS.

2) No deduction in respect of any expenditure other than cost of acquisition shall be allowed while computing the income from transfer of virtual digital currency.

3) Accordingly, brokerage and other charges have not been considered.

4) No other loss or allowance can be set off against gains from transfer of virtual digital currency. Accordingly in case 2, loss from sale of shares of Infosys amounting to INR 200,000 is not available to be set off against the gains of INR 300,000 from sale of bitcoin.

5) Further, loss from sale of virtual digital currency cannot be carried forward to subsequent tax years.

6) Also, as per the proposed amendments, the bitcoins worth INR 200,000 shall be offered to tax by Subhash, under the head IFOS while filing his individual tax return.

The amendment is a welcome step for bringing clarity in the taxation aspect. However, it is pertinent to note that trading/ dealing in cryptocurrency has not been legalized in this budget. There is clarity awaited in such regards.

Key points that still require clarification from government

While a scheme of taxation has been provided for VDA, there are still certain ambiguities around the VDA taxation.

1) While taxation of transfer of VDA has been clarified, there is no clarity on taxation of activities such as development and creation of VDA.

2) If a person pays for a good or service in cryptocurrency, whether payment will be considered as a mode of settlement or as sale of cryptocurrency to another person against consideration of goods or services. This leads to the question of whether the purchaser of goods/ recipient of services will have to pay taxes separately on this transaction by considering it as a ‘transfer’ of VDA. Whether the seller of goods/ provider of services will have to deduct TDS while receiving the payment through VDA.

3) Cryptocurrencies are mostly bought and sold in foreign currency. Accordingly, an increase or decrease in value of the rupee will also result in fluctuation in gain or loss. How are gain/loss arising from forex fluctuation to be treated?

While the Government has clarified its stand from the Income Tax perspective, no clarity has been provided with respect to Crypto Currencies from a GST standpoint. There are various aspects on which clarity is required under GST Law so that investors are sure of the GST implications and are able to make more informed decisions. Primarily, below are some of the major area where Government needs provide to clarity:

a) Whether GST is applicable?

b) If yes, the nature of Cryptocurrencies – whether goods or services?

c) GST implication on transaction fees/ rewards to miners, Exchanges where the consideration is paid in cryptocurrency.

d) GST implication where cryptocurrency is used for acquiring goods or services

e) Government is likely to introduce legislation on cryptocurrencies which will provide a framework as to how the cryptocurrencies and usage thereof will be regulated. It is also expected that along with that the government should provide definitive guidance from a GST perspective including the above mentioned points.

This article was originally published on The Times of India.