Healthtech start-ups showing positive intent amid funding challenges

Article

By: Bhanu Prakash Kalmath S J

08 Dec 2023 2 min read

The healthtech start-up landscape in India experienced a significant boost in funding and company growth, largely driven by the impact of the pandemic. With a population exceeding 1.4 billion and an escalating demand for healthcare services, investors are identifying lucrative opportunities in the healthtech sector. Leveraging India's robust IT capabilities, these start-ups are revolutionising healthcare through innovations like telemedicine platforms, tele-radiology, home healthcare solutions, artificial intelligence (AI)-driven diagnostics, and advanced health information systems. Telemedicine, in particular, has emerged as a transformative force, enhancing accessibility and saving time and costs, especially in rural areas.

Simultaneously, the government recognises technology as a pivotal tool to achieve universal health coverage. The collective efforts under Ayushman Bharat Digital Mission (ABDM) and eSanjeevani underscore the government’s dedication to harnessing technology. The Union Budget 2023-24 further includes several provisions aimed at promoting digital innovation to enhance the accessibility and affordability of healthcare, such as the establishment of AI centres of excellence and 100 labs for advancing 5G services.

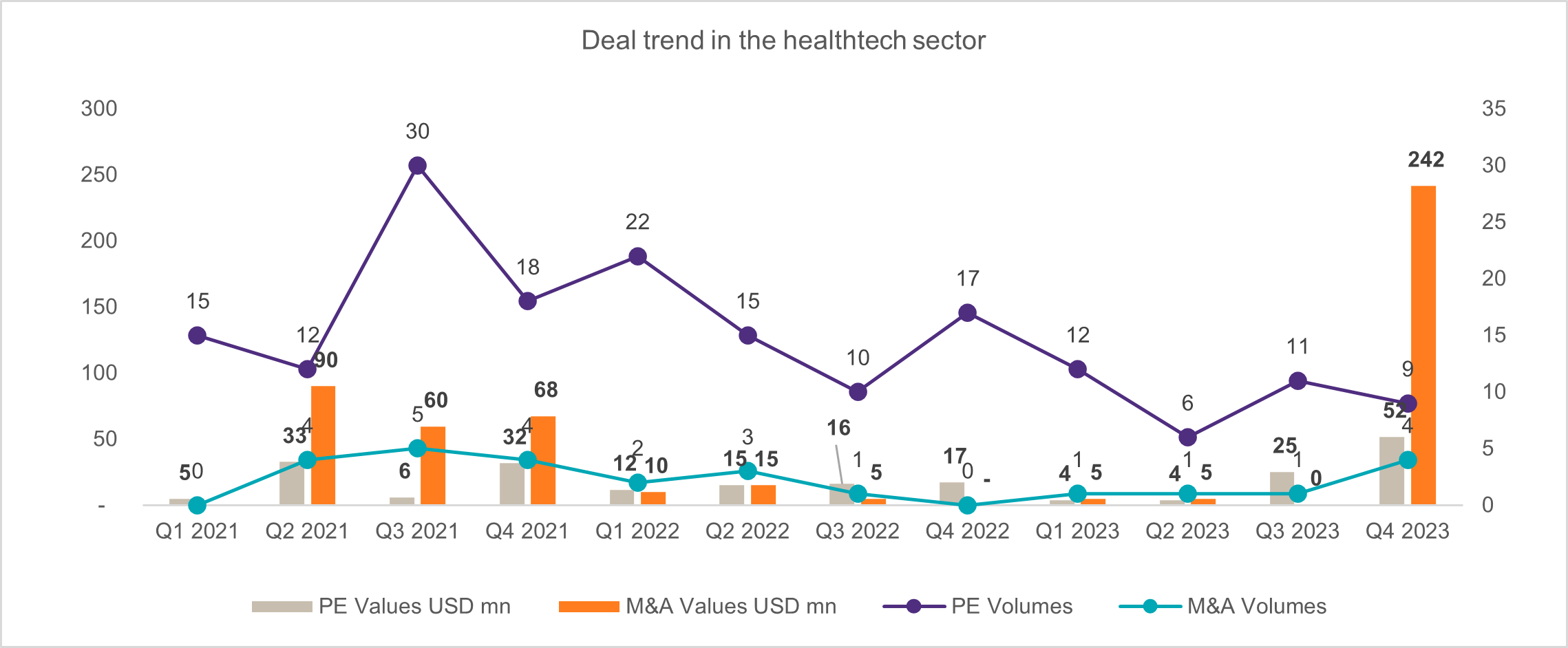

Although the private sector dominates healthcare in India, healthtech start-ups have faced funding challenges over the past two years. Deal trends in both mergers and acquisitions (M&A) and private equity (PE) have been dynamic. After an overall downward trend from the second half of 2021 to 2022, the M&A deal trend witnessed a significant increase in both volumes and values in the latest quarter, Q4 2023, indicating a robust and active market. The steady rise in M&A volumes suggests a positive trajectory, possibly fuelled by market confidence and strategic business decisions.

PE activities, on the other hand, witnessed an overall decline in volumes after a peak of 30 deals witnessed in Q3 2021, attributed to factors like the ongoing funding challenges, economic slowdown, and a shift in investor preferences influenced by rising interest rates. Despite this decline, notable investors like 9Unicorns, Y Combinator, Sequoia Capital, Temasek, Quadria Capital, and Accel Partners remained active in the sector, reflecting ongoing interest.

Source: Grant Thornton Bharat Dealtracker

Despite these challenges, the future outlook for healthtech start-ups appears positive. Reports indicate that the healthtech market had an estimated size of USD 10.6 billion in 2022 and is projected to reach USD 21.3 billion by 2025. Various factors contribute to this growth, including rising income levels, an ageing population, increased internet and smartphone penetration, heightened government spending on digital infrastructure, greater health insurance penetration, and collaborations between healthcare providers and tech companies, collectively driving the expansion of the healthtech ecosystem.

Addressing the substantial demand-supply gap in healthcare, technology, particularly AI, holds the potential to bridge the ‘missing middle’ in India. Technology plays a crucial role in preventive healthcare, offering solutions such as early detection and screening, telemedicine, mobile health applications, smart wearables, and fitness trackers that encourage healthy lifestyles and disease prevention.

While technology holds immense potential to advance universal health coverage and drive the growth of the healthtech industry, it comes with the responsibility of handling personal health data appropriately. The new Digital Personal Data Protection Act (DPDPA), 2023, emphasises the importance of safeguarding personal data, providing an opportunity to build consumer trust for future growth. Ultimately, Indian consumers stand to be the biggest beneficiaries of the growth of healthtech in India.

Authors

-

Bhanu Prakash Kalmath S J

Partner and Healthcare Services Industry Leader