COVID-19: Managing valuation challenges for private equity funds

18 Jun 2020The impact of COVID-19 has been felt globally across countries, business houses, capital markets, private and public sector entities. India is now on the verge of gradually and cautiously unlocking the economy after industries and business operations have been under lockdown for almost three months.

Among other financiers and investors, the fourth wheel of the finance industry, private equity (PE) and venture capital (VC) funds, are also witnessing huge challenges. Given the turmoil in the global economy, such funds face an uncertain road to recovery in the coming months.

Impact of COVID-19 on PE, M&A deals and stock markets

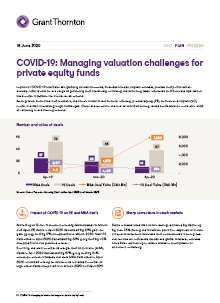

According to Grant Thornton’s monthly deal trackers for March and April 2020, PE deals in April 2020 decreased by 27% year-on-year (y-o-y) and by 17% compared with March 2020. Total PE deal value in April 2020 decreased by 63% y-o-y and by 40% compared with the previous month.

Similarly, total number of M&A deals in April 2020 decreased by 57% y-o-y and by 24% month-on-month. However, total M&A deal value in April 2020 increased by around 4-times, from USD 1.8 billion to USD 7.9 billion mainly on account of increased number of high value deals compared with March 2020 and April 2019.

Banking and financial services sectors have been severely affected. P/E and P/B multiples of the Nifty Bank index decreased by 49% and 47% respectively, between December 2019 and March 2020.

Here’s how PE leaders can PLAN to manage their valuation challenges and ascertain the appropriate value of unlisted stock

Valuation through transaction price

- The pre-COVID-19 transaction price needs calibration with market inputs at the time of investment and on the valuation measurement date.

Consider comparable companies’ multiples:

- Comparable company multiple method as on the valuation measurement date uses financial metrics of the last reported quarter. Hence, it does not capture the realistic expected run rate, given the current disruptions in the business cycle.

Explore discounted cash flow method under the income approach

- Care should be taken to avoid double dip i.e. increased discount rate for uncertainty and revised lower financial projections adjusted for uncertainties.

and more..