COVID-19: Impact on shadow banking sector

15 Jun 2020The COVID-19 pandemic poses unprecedented challenges related to health and economic/financial stability. While the priority is to save lives, the necessary containment measures have led to dramatic decline in economic activity.

As a result, in only three months, the 2020 outlook has shifted from expected growth of more than 3% globally to a sharp decline of 3%, which is much worse than the output loss seen during the 2008-09 global financial crisis. The ultimate impact on the world economy as well as recovery time is highly uncertain.

Some of the key measures announced by the Reserve Bank of India and the government to mitigate impact of the pandemic on businesses have been the following:

- 6 month moratorium on EMIs

- Refinancing facilities for all India financial institutions such as the NABARD, SIDBI and NHB

- Constant reduction in repo rates under the liquidity adjustment facility

- Second tranche of targeted long-term repo operations (TLTRO 2.0) for an aggregate amount of INR 50,000 crore

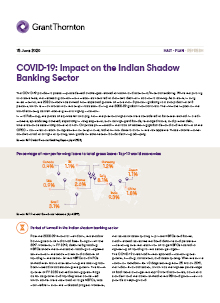

Impact on NBFCs and HFCs

Overhauling the business model

- Owing to disruption due to the pandemic, companies have to adapt to the new normal, which would, in turn, lead to a recalibration of every model and processes

Liability impact

- Although measures by the RBI would help in facilitating liquidity to the sector, it may not lead to credit flow in the economy as the lending institutions would prioritise liquidity over balance sheet growth

Collection impact

- Lending institutions are likely to observe heightened delinquencies in second and third quarters (after the expiry of the moratorium) as the halt in business activity due to the lockdown would severely impact cash flows of the borrowers

Reporting impact

- Banks follow Indian GAAP, whereas NBFCs and HFCs follow Ind-AS. The difference in quantification and reporting of ECL is likely to have a severe impact on the results of the lending institutions

and more….