Budget 2022: top changes in personal tax

Union Budget 2022

By: Akhil Chandana

01 Feb 2022 3 min read

Budget 2022 was announced amidst high expectations from all sides. The Budget focuses on trust-based governance, standardisation of taxation provisions and reduction of overlapping compliances under various laws. Let us look at the key Budget 2022 tax proposals which impact individual taxpayers.

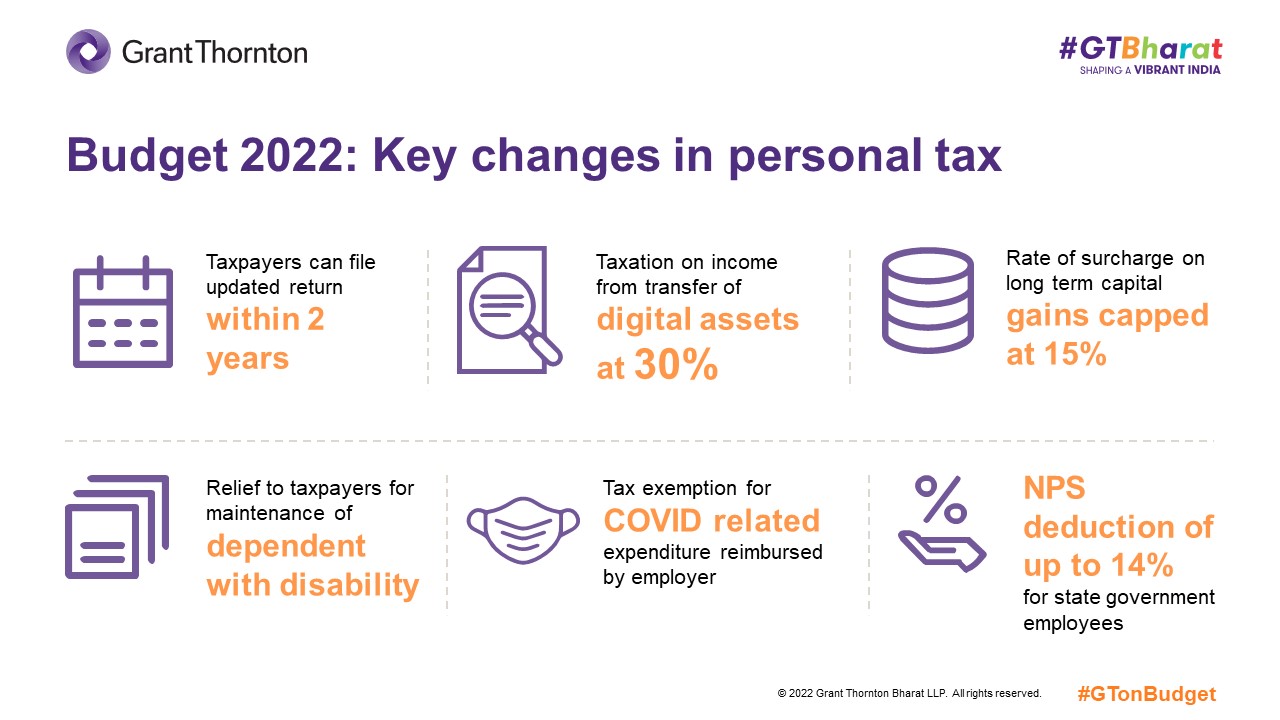

- Facility for filing updated tax return: With an intent to encourage voluntary compliance and reduced litigation, a new concept of Updated Return has been introduced. Taxpayers can file an updated return to voluntarily disclose income which was either under reported or not reported at all in any tax return. The updated return can be filled within two years from the end of relevant assessment year subject to certain conditions. An additional tax of 25% or 50% of the tax and interest due on the additional income being reported would be payable on such income.

- Introduction of taxation scheme for virtual digital assets: Transactions in virtual digital currencies and assets have seen an upswing in recent years and this was a step to provide a mechanism for taxing income from such transactions. Any income from the transfer of virtual digital assets is proposed to be taxed at 30%. Only the cost of acquisition of such asset would be allowed as a deduction while calculating the taxable income. Further, any loss arising from transfer of such assets would not be allowed to be set off against any other source of income.

![NDTV_Personal-Tax-1.png]()

With a view toward having a transparent tax regime and capture details of such transactions, TDS at the rate of 1% on such transfers has also been proposed. Also, any gift of such assets will be taxed in the hands of recipient. This provides certainty to a large section of individual taxpayers who have invested in digital currency, though a lower rate of tax would have been welcome.

- Capping of rate of surcharge on long term capital gains: As per the existing provisions, long-term capital gains on listed equity shares, equity oriented mutual fund units, etc. are liable to maximum surcharge of 15%, while the other long term capital gains are subject to a graded surcharge which may go up to 37%. Budget 2022 has proposed capping of surcharge rate at the rate 15% in case of all long-term capital gains. This will benefit taxpayers in higher income brackets who were earlier liable to surcharge at the rate of 25% or 37% on such gains.

- Relief to taxpayers for maintenance of dependent with disability: The present law provides for deduction to a taxpayer for amount paid towards an insurance policy for the benefit of a disabled dependent only if the lumpsum payment or annuity is available to the disabled person on the death of the taxpayer. It is proposed to extend the deduction with respect to such scheme as well where the lumpsum or annuity is receivable by the taxpayer upon attaining age of sixty years.

- Tax exemption for COVID related expenditure reimbursed by employer: Any sum paid by the employer for any expenditure actually incurred by an employee on their medical treatment or treatment of any family member in respect of any illness relating to COVID-19 would not be considered as a taxable perquisite, subject to such conditions as may be notified by the Central Government. Important to note that the press release to this effect had been announced in June 2021 and amendment in tax laws were awaited.

- Rationalisation of NPS provisions: To bring parity with central government employees, the benefit of deduction u/s 80C for employer’s contribution to NPS up to 14% of salary has been extended to state government employees as well. The exemption limit for employer contribution to NPS in case of employees in private sector remains at 10%.

While the Budget 2022 gave a miss to popular expectations such as increase in standard deduction and limit for section 80C which were expected to result in more cash in hand for the common man, there are some proposals on the anvil which will benefit various sections of individual taxpayers.

Authors

-

Akhil Chandana

Partner, Tax, Grant Thornton Bharat