This year, India rose 14 places to the seventh rank on the protection-of-minority-investors’ list, a silver lining to the gloomy larger picture of the country sliding to the 142nd position on the overall list in terms of doing business.

However, with several rollbacks and postponement of reforms announced, following complaints from companies, India might struggle to maintain its position when World Bank revisits the index next year.

Nadine Abi Chakra, co-author of the report, told Business Standard India’s score in terms of protection of minority investors increased due to the Companies Act, 2013, and the introduction of new indicators. “India is, in fact, ranked first on the shareholder governance index. It is 27th in terms of conflict of interest regulation, as a result of the Companies Act, 2013. Overall, India improves from 21st (DB2014 back-calculated) to seventh in the rankings,” she said.

This year, the authors of the report changed the name of the ‘protecting investors’ indicator to ‘protecting minority investors’ to better reflect the indicator’s scope. As a result, three indices were added to gauge protection in matters beyond conflict of interest. And, the existing ease-of-shareholder-suits index was expanded to take into account the allocation of legal expenses.

M P Vijay Kumar, chief financial officer of Sify Technologies and author of several books on company law, said reforms in the Companies Act were key to the jump in rankings. He identified 10 key areas in which the new law had enhanced minority investor protection (See box: Key reforms in Companies Act, 2013). But consultants such as Yogesh Sharma, assurance partner, Grant Thornton India LLP, feel some of the stringent provisions introduced to protect minority investors are “so strict that perhaps, these are harsher than in some of the most advanced capital market jurisdictions”.

Such complaints by consultants and corporations led to a rethink in the Ministry of Corporate Affairs. Since June, the ministry has announced at least two rounds of dilution in the definitions and norms governing related-party transactions. Proxy advisory firms had pointed out instances in which some companies that would have required ‘majority of minority investors’ nod’ for a related-party transaction escaped the provision due to relaxation in the Act.

Some changes in the methodology that went India’s way:

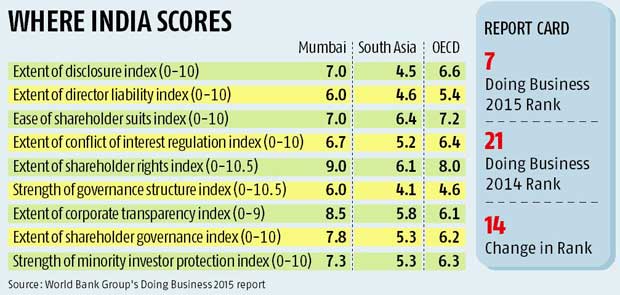

A new indicator was added to gauge corporate governance beyond related-party transactions. The extent of shareholder governance index encompasses a range of issues and data:

- Shareholders’ rights and role in major corporate decisions: The extent to which shareholders can influence important corporate decisions such as appointing and removing board members, issuing new shares and amending the company’s by-laws and articles of association (score 0-10.5)

- Governance structure: The extent to which the law mandates separation between corporate constituencies to minimise potential agency conflicts. The issues covered included whether the chief executive could also be chairman of the board of directors, whether the board must include a minimum number of independent directors, and whether there were rules relating to cross-shareholding and subsidiary ownership (score 0-10.5)

- Transparency: The extent to which companies are required to disclose information about their finances, the remuneration of their managers and directors, and their other directorships (score 0-9)

India scores

- 9 out of 10.5 on the shareholders’ rights index

- 6 out of 10.5 on the strength of governance structure

- 5 out of 9 on the extent of corporate transparency

- India scored 7.8 on the shareholder governance index, an average of the three scores

Further, the Securities and Exchange Board of India, which had strengthened its corporate governance norms in April, also revised the regulations and announced changes in September, just a fortnight before it was to be implemented on October 1.

The Doing Business 2016 report, to be published next year, will assess the impact of reforms and amendments implemented between June 2 this year and June 1, 2015.

Chakra doesn’t rule out the possibility of negative amendments affecting the rating. “In fact, during each cycle, the Doing Business report team takes note of reforms – negative or positive – implemented by economies around the world and assesses their impact on the data.” Chakra added, the data came from a questionnaire to corporate and securities lawyers and were based on securities regulations, company laws, civil procedure codes, court rules of evidence and all amendments thereof.

During each cycle, the indicators on protecting minority investors ascertain minority shareholder protection against directors’ misuse of corporate assets for personal gain. They also gauge other aspects of corporate law that are unrelated to this transaction but indicative of the protection of minority shareholders.

Sharma of Grant Thornton said the rollbacks might not significantly impact the rankings adversely next year. “It is worth citing, none of these exemptions and relaxations (including proposed ones) will hamper the interest of investors or the public at large, as these cover only private companies and companies with no or very low public interest.”

He added, the underpinning idea behind some of the recent amendments, was providing practical relief to companies facing challenges in implementation, the cost of which might have outweighed the benefits.

Key reforms in companies act, 2013

- Giving dissenting shareholders an exit opportunity: Section 27 of the Act provides dissenting shareholders an exit opportunity if they do not agree to any terms of contracts or objects referred to in the prospectus

- Protection from variation in shareholder rights: If the share capital of a company is divided into different classes of shares and a variation in the rights of shareholders is proposed, holders of at least 10 per cent of the issued shares of a class who do not agre to such variation may apply to the tribunal for cancellation of the variation, under Section 28

- Enforcement of shareholder agreements: Section 58 provides for enforcement of shareholder agreements. As the Act has specifically validated the idea of entrenchment, all contractual agreements by shareholders now have legislative recognition.

- Resolutions requiring special notice: Under section 115, for any resolution requiring a special notice, a notice must be given to the company by members holding at least one per cent of the total voting power, or those holding paid-up shares of an aggregate sum of not more than Rs 5 lakh

- Highlighting profit or loss attributable to ‘minority interest’: During the preparation of consolidated financial statements, the profit or loss attributable to ‘minority interest’ and to owners of the parent, shall be presented as allocation for the period. The ‘minority interest’ in the balance sheet within equity is to be presented separately from the equity of the owners of the parent

- Listed companies to appoint directors elected by small shareholders: The Act has sought to empower minority shareholders in corporate decision-making. Section 151 requires listed companies to appoint directors elected by small shareholders holding shares of a nominal value not exceeding Rs 20,000

- Exit route for dissenting shareholders: Under Section 230, dissenting shareholders in terms of a resolution seeking approval for a scheme of arrangement or compromise involving any class of creditors or members may be granted exit offers, if recommended by the relevant authority

- Purchase of minority shareholding: The Act explicitly deals with the issue of buying out minority shareholders of a company, under Section 236. This provision was absent in Companies Act, 1956

- Class action suits: The Act specifically provides for class action suits (under Section 245) brought by: (i) members or (ii) depositors of a company, in case they feel the management or conduct of the affairs of the company is in a manner prejudicial to the interests of the company or its members or depositors

- Independent directors to safeguard interests of minority shareholders: Under the code for independent directors, it is mandatory to protect the interests of minority shareholders

Shriram Subramanian of Ingovern Research Services, a proxy advisory firm focusing on minority investor issues, says, the rollbacks in reforms may not affect the rankings significantly. “Some norms apply, as they have enhanced corporate governance; others have subsequently been diluted or postponed. Still, we have made progress in the positive direction,” he said.

According to experts, implementation of these provisions would be important for the ranking. “As far as the ranking goes, I think it will really depend on how effectively the government monitors the compliance with the new law,” said Sharma of Grant Thornton.

The article appeared in the Business Standard. The article can be found here.